Mortgage rates are a popular topic online and in the news. These days, information travels fast and everyone seems to be an expert on the topic of mortgage rates. The trouble with all this information flying around is that much of it is inaccurate, or out of date. This is especially true with the internet and the media and their reporting on MORTGAGE RATES.

HERE ARE SOME VERY COMMON EXAMPLES…

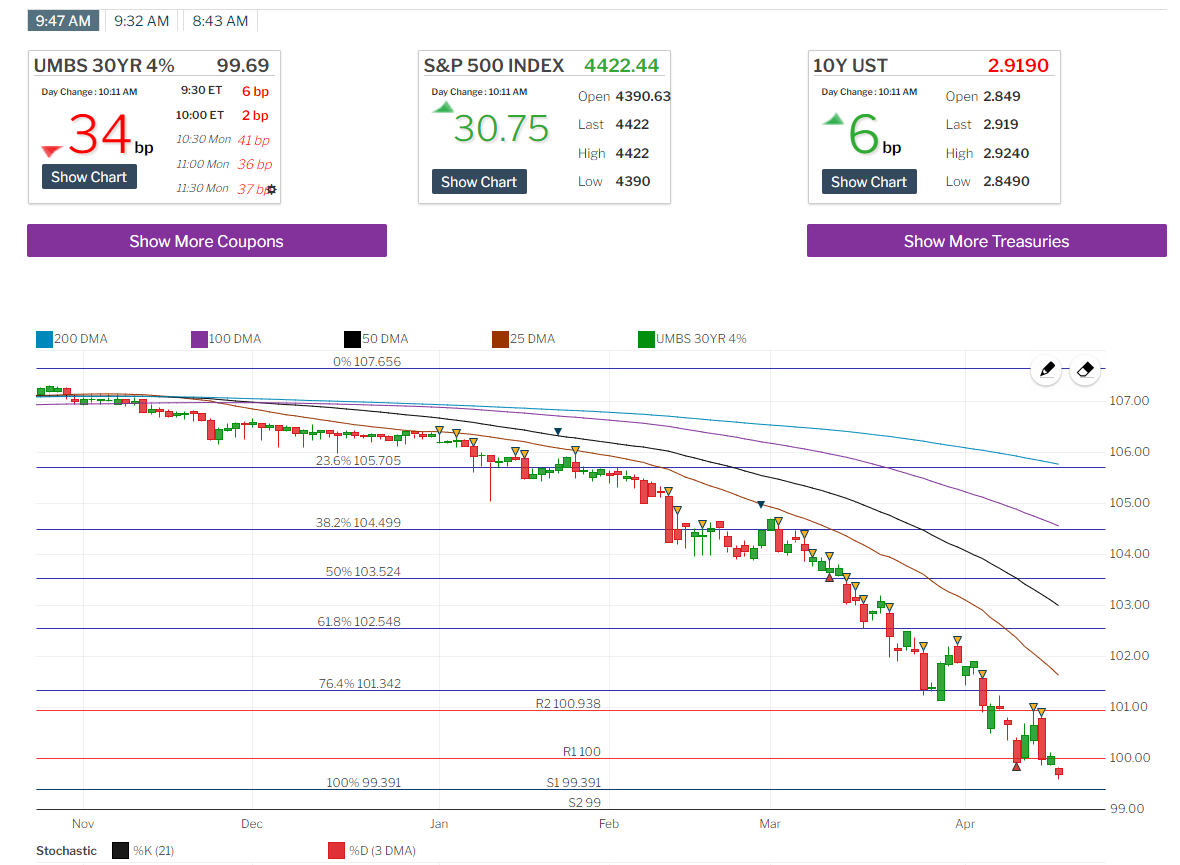

****Mortgage rates are based on the 10 year treasury – Wrong! We hear this all the time from people who are supposed to be experts. Mortgage rates are directly impacted by the price of mortgage bonds, also called mortgage-backed securities (MBS). Treasuries and MBS most of the time move in similar directions since they both trade in the bond market, however it’s not uncommon for treasuries and MBS to move in opposite directions, or be very disconnected.

Below is a screen shot of mortgage-backed security bond trading that we use to track the movement of bond prices to see where rates are heading. There are many different technical factors on this chart that the average person might get confused with, so I will spare you the nerd talk and put this in simple terms. The easiest way to read this chart is “green is good” and “red is bad”.

As the price of a bond rises, yields (rates on mortgages) will fall. Inversely, if bond prices decline, rates will rise. Lenders & banks adjust their rates daily based on these bond prices. It’s also not uncommon that on very volatile days, rates may change multiple times in a day. This is why rates are a moving target for everyone. It’s never set in stone until the rate is locked.

****Freddie Macs weekly survey says 30 year rates fell this week – This could be right or completely wrong. The survey is completed Monday-Wednesday each week, with the surveyed lenders sending in their rate quotes whenever they please, as long as the quote is delivered by Wednesday evening. The results are averaged and then issued to the public on Thursdays. By the time the report has been issued on Thursday, rates could have improved, or worsened every day. This data is also still based only on quotes, so this is only what the lender would quote at that exact time on that exact day to a borrower who met certain criteria. Again, these are quotes, not confirmed rates that were actually locked and settled.

These rates quotes from the surveyed lenders make the following assumptions:

- Conventional loans only

- The customer is paying an average of .5 points to obtain that rate

- The lock period is based on 30 days only

- 740 or higher credit score for all applicants

- Loan to value of 80% or less (on a purchase that means no less than 20% down)

- Conforming loan amounts only (based on county limit)

- Single family 1 unit home (not condo) (not 2-4 unit)

The Freddie Mac survey does give the general public some information as to the trend of mortgage rates from week to week, but as we already established, their data is compiled over several days, making a lot of the data inaccurate by the time the rate average is broadcast to the general public. On many occasions, the news report on the survey is opposite of the real market.

****Actual reported news online: 30 year mortgage rates fell 7 basis points from 5.07% to 5.00%.

Decoded: This actually means that rates fell from around 5% to still around 5%. 5.07% is still essentially 5% as it translates to a quoted rate. The news leads everyone to think rates really fell, but in fact, they did not really move at all.

****The Federal Reserve increases rates – This is only partly correct. The Federal Open Market Committee or better known as the “FOMC” or the”Fed” does not set mortgage rates directly, but they do set the Federal Funds Rate. This is the rate that banks charges each other to borrow funds overnight. Any time that the Fed changes the fed funds rate, many other lending rates and indexes move in lockstep, meaning they move up or down by the same amount. This includes the Prime rate, which directly impacts home equity loans, car loans and personal loans. As the fed funds rate rises, borrowing costs for consumers across the board rise. This does not directly impact MBS and mortgage rates, however, the reaction of the market could have a negative or positive impact on the price of MBS and mortgage rates. Since investors typically purchase bonds (Treasuries, MBS, etc.) when there is a flight-to-safety out of equities (stocks), the news, economic reports, or even just an announcement by the fed can indirectly push mortgages rates in either direction at any time.

****My credit union or online lender is offering a lower rate – This is something that we hear all the time. At the time that we hear this, we likely have already provided the customer with a fully itemized mortgage estimate based on their loan option preferences. The customer in many cases may have found some mortgage rates listed online for a program with a similar name and then they assume that the lower rates online are what they should qualify for. Then, we take the time to explain why comparing our estimate to those online rates is not an apples to apples comparison.

****Recently, a customer said that he was going to switch to an online lender who quoted him a lower rate of 4.875% vs. our rate of 5%. What he failed to realize is that this rate that he was quoted was not all it was cracked up to be. When he was directed by us to click on the list of assumptions associated with this quote, he found out that the quote was based on 25% down, a 740 credit score and paying 2.25 points at closing. In fact, he was actually trying to obtain a loan with 20% down, he had a 739 credit score and we were not charging him any points. Before we saved him, he was about to pay thousands of dollars more just to save around $30/month.

These examples are very common, but they can be avoided. When you are rate shopping or comparing lenders, just be sure that you are comparing apples to apples. At any given time a comparison of rates could be .125% different depending on when each estimate was prepared, but if one rate quote is much lower, there is likely something else going on that has not been disclosed yet and buyer beware.

You may be able to find a lower rate when you venture out on the internet, but cheap advise can be more costly in the long run. The best policy is to make sure you are working with a seasoned mortgage professional.

I hope you found this information to be useful. Please add comments or questions or you can contact us directly for additional clarification on these subjects.

QUESTIONS?

Click HERE to connect with us, or to have us contact you

Curious if you qualify? – Call or email us directly, or Pre-Qualify Here

Call us at (240) 670-5090 or email us at CJMT@mainstreethl.com